Friday, April 28, 2006

Buying real estate for nothing down still possible

Here is a column about buying homes with "nothing down" ...Several methods help minimize costs, maximize benefits

Friday, April 28, 2006By Robert J. BrussInman News"Is it really possible to buy a house for nothing down?"That is the question I was asked by a "twenty-something" young lady at a cocktail party I recently attended.My reply was, "Absolutely, yes." But then I quickly qualified that statement by adding she needs good income and good credit. Her husband, standing nearby, perked up at that point and suddenly became very interested in the conversation.Then I regaled them with brief stories of how I bought my personal residence and several rental houses for nothing down. I hope I inspired them to move out of their expensive luxury city apartment and buy their first home.As I left that conversation, my parting words were, "Your first home won't be your ultimate dream home. But it will be a start toward eventually buying your perfect home."Personally, the first "nothing down" residence I bought was a modest two-bedroom house, which, looking back, I would now classify as a "major fixer-upper." It was far from perfect, but it was a start.What does "Nothing Down" mean?The simple definition is "zero cash from your pocket to buy your home." However, that definition does not mean the home seller won't receive cash from the sale. In fact, the seller often receives 100 percent cash in a nothing-down home purchase.If you have good income and good credit, mortgage lenders are thrilled to loan you 100 percent of your home's purchase price. But it won't be cheap!Lenders usually charge a slightly above-market interest rate for zero-down-payment mortgages. In addition, they require PMI (private mortgage insurance), which requires a monthly premium to protect the lender's top 20 percent, or riskiest part, of the mortgage. PMI premiums are not inexpensive, so be prepared.If you are a bit short of cash, the nation's largest secondary mortgage market home loan lenders, Fannie Mae and Freddie Mac, will even loan up to 103 percent of your home's purchase price to help pay the closing costs. Just to be sure you can qualify for a 100 percent home loan, it's smart to shop for a mortgage before you shop for a house or condo. Then you can receive a written pre-approval from an actual mortgage lender (not just pre-qualification, which means nothing) so you will know your maximum mortgage amount.

Why smart home buyers purchase for little or no cash.There are two major reasons for buying a house or condo for little or no cash:

1.) YOU DON'T HAVE THE DOWN PAYMENT CASH.

Just because you are "cash challenged" is no reason not to buy a house or condo. Even if you have lots of cash, why tie it up in your residence? There are many ways to buy a home for zero cash.

2.) YOU ARE A VERY SMART HOME BUYER WHO UNDERSTANDS LEVERAGE BENEFITS.

The second major reason for buying a home with little or no cash is to maximize your leverage benefits. To illustrate, suppose you buy a $300,000 house for $300,000 cash and that house appreciates in market value at the historic nationwide average rate of 5 percent annually. In 12 months, it will be worth $315,000, or a 5 percent yield on your investment. Instead, suppose you obtained a $300,000 zero-down-payment mortgage and the house rose 5 percent in market value in the next 12 months. Yes, you had to pay monthly mortgage payments, roughly the equivalent of rent. But now you "earned" $15,000 on zero investment for an infinite yield.

Creative ways to buy for zero cash down payment Presuming you want to buy your next house or condo for little or no cash, there are many ways to do so. The most obvious is to obtain a 100 percent or greater new mortgage. But this method requires good income and good credit, and it can be expensive.Instead, suppose you don't need 100 percent financing, but you don't want to tie up a bundle of down-payment cash. The first step is to get pre-approved with a mortgage lender for the maximum mortgage you can obtain. Be sure this approval is in writing from the actual lender, not a worthless "pre-qualification letter" from a mortgage broker.The second step is to use that written lender's mortgage pre-approval to buy the home you want. If you keep the mortgage balance below 80 percent of the home purchase price, you have many alternatives:One is the 80-10-10 plan where you obtain an 80 percent first mortgage, a 10 percent second mortgage, and pay a 10 percent cash down payment.Another is 80-15-5 where you pay only 5 percent cash down payment and either the seller carries back a 15 percent second mortgage or the lender arranges a 15 percent second mortgage home equity loan. Either way, you receive maximum leverage benefits, buy your home for practically nothing down, and avoid costly PMI premiums.

Finance first, them buy your home for little or no cashAfter pre-arranging your home mortgage, and getting a written pre-approval letter or certificate from the actual lender, it's time to start shopping for a house or condo. However, in the back of your mind, be sure to consider how much home you can afford.Armed with the confidence of a written pre-approval letter from a mortgage lender, you can decide what zero- or low-down-payment choice you prefer. When you see the home you want to buy, this is no time for the "paralysis of analysis."With the help of your experienced buyer's agent, make your purchase offer before another buyer steals your home. However, be sure your purchase offer contains two key contingency clauses for 1) a satisfactory appraisal of the home, as required by your mortgage approval letter, and 2) a professional home inspection.Unless you got carried away and offered too much for the house or condo, the appraisal contingency should not be a problem. However, the home inspection is vital. Be sure to accompany your inspector to be certain there are no latent or surprise home defects discovered.If your inspector discovers a serious undisclosed home defect, then you can either negotiate for a "repair credit" toward your purchase price or cancel the sale and obtain a refund of your earnest money deposit if the seller refuses to be reasonable. More details are in my special report, "Secrets of Buying Your Home or Investment Property for Nothing Down," available for $5 from Robert Bruss, 251 Park Road, Burlingame, CA 94010 or by credit card at 1-800-736-1736 or instant Internet delivery at www.BobBruss.com.Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

Thursday, April 27, 2006

Economists: Housing Market Hasn't Gone Flat

Here's a portion of an article from the New York Times ...Vikas BajajThe New York TimesThursday, April 27, 2006As the first quarter of 2006 ends, economists are generally upbeat about both the economy and the housing market.''Neither the economy, nor the housing market has gone flat,'' says Stuart G. Hoffman, chief economist for the PNC Financial Services Group. ''But it will continue to deflate a little bit.''The market was weaker when compared with a year ago. The home selling rate in March was down from a pace of 1.31 million in March 2005, while the median price slipped 2.2 percent from a year ago, to $224,200.And the number of unsold homes on the market has grown, rising by 24.4 percent over the last 12 months, to 555,000. At the current sales pace it would take five and a half months to sell those properties, up from 4.2 months a year ago.The jump in inventories was the biggest in 33 years, and the drop in prices the steepest since January 2003, says Ian C. Shepherdson, chief United States economist at High Frequency Economics.Sales ''are going to drop in the next couple of months,'' he said, noting that mortgage applications, an early indicator for the housing market, have fallen 22 percent in 12 months.Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

Survey: Internet, real estate agents are key to finding homes

Here's an article about the best way to find the perfect home ...Photos, maps popular in online searches

Wednesday, April 26, 2006Inman NewsMost home buyers first learned about the homes they purchased through a real estate agent or the Internet, according to a survey conducted for Prudential CA/NV/TX Realty, while 5 percent of respondents said they discovered the properties in a newspaper.About 18 percent of respondents said they found the home they purchased by viewing a yard sign or driving by the home, and 9 percent said they learned about the home through a friend.About 36 percent of buyers who bought a home in the last three years said they first learned about the properties from their agent, while 31 percent of buyers said they learned about the properties through the Internet, according to the telephone survey.The survey is based on responses from 300 adults living in private households in Northern California who purchased a home in the past three years and used the Internet to search and view homes."Agents remain an essential source of information for consumers, but the relationship is changing as agents play more of a consulting role," said Sherry Chris, chief operating officer of Prudential CA/NV/TX Realty, in a statement.When buyers were asked to identify the most important reasons for visiting a real estate Web site, the top three responses were: "looking at property photos," 89 percent; "property search," 85 percent; and "mapping a property," 77 percent.Less popular responses included finding "financing information," 31 percent; "locating an agent," 26 percent; and "career information," 11 percent.About 91 percent of respondents said they most enjoyed using the Internet for their home search because "it saves time," while 45 percent said "it empowers you in the transaction."Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

Wednesday, April 26, 2006

JUST LISTED! 8126 Palm View Lane, Orangecrest

NOW PENDING! IN ONLY 8 DAYS!

Beautiful, tastefully upgraded home in wonderful Orangecrest Country, one of the most sought-after neighborhoods in Riverside. This gorgeous home boasts elegant distressed hardwood flooring, upgraded carpet, baseboards, custom paint, canned lights with dimmers throughout, granite countertops, a butler’s pantry and plantation shutters throughout. Through the sliding glass door from the kitchen you have access to a great patio in a private manicured back yard. Pride of ownership is more than apparent in all of the details. Beautiful, tastefully upgraded home in wonderful Orangecrest Country, one of the most sought-after neighborhoods in Riverside. This gorgeous home boasts elegant distressed hardwood flooring, upgraded carpet, baseboards, custom paint, canned lights with dimmers throughout, granite countertops, a butler’s pantry and plantation shutters throughout. Through the sliding glass door from the kitchen you have access to a great patio in a private manicured back yard. Pride of ownership is more than apparent in all of the details.

Bedrooms: 5. Baths: 3. Home size: 3,288 sf. Lot size: 0.17 acre. Year built: 2001. Swimming Pool: No. Garage: 3-car. List Price: $619,900

Your home could be next. To get a free market analysis, or for other local real estate information, call Scott Chappell & Brian Bean’s 24-hour hotline at (800) 941-1900. It’s a community service offered by one of Orangecrest’s leading real estate teams.

Ask about Scott & Brian’s 100% Satisfaction Guarantee program. If you aren’t satisfied, they’ll refund their commission.

Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

JUST SOLD! 19818 Allenhurst St., Orangecrest

Amazing Orangecrest pool home! Whether entertaining or enjoying a peaceful evening, you can find your very own piece of paradise right here. The magnificent floor plan boasts a large kitchen, featuring an island equally suited for holiday banquets or intimate dinners. Relax and enjoy the soothing sounds of your rock-feature waterfall or lounge in the spacious comfort and warm colors of your own private escape.

Bedrooms: 4. Baths: 3. Home size: 2,790 sf. Lot size: 6,969 sf. Pool: Yes. Year built: 2001. Garage: 3. Sales Price: $599,900. Days on Market: 83.

Your home could be next! To get a free market analysis, or other local real estate information, call Scott Chappell & Brian Bean’s 24-hour hotline at (800) 941-1900. It’s a community service offered by one of Orangecrest’s leading real estate teams.

Ask about Scott & Brian’s 100% Satisfaction Guarantee program. If you aren’t satisfied, they’ll refund their commission.Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

Single mom seeks loophole in $250K home-sale exemption

Here's a column with some vital information ...Can woman add teenage son to home title for extra tax savings?

Wednesday, April 26, 2006By Robert J. BrussInman NewsDEAR BOB: I am a single mom struggling to make ends meet. Fortunately, I bought my home in 1999 for $315,000. Today, it is worth close to $700,000. I am considering selling and moving to a smaller home in a less-expensive neighborhood, hoping to eliminate the mortgage payments.But I was recently dismayed to learn that because I am single I can only exclude $250,000 profit from capital gains taxes, while my friends who have husbands can exclude $500,000. Is there any way around this limitation? Can I add my son to the title when he turns 18? Would it be wiser to sell my home without making costly cosmetic upgrades such as new carpet and paint? -- Cathy J. DEAR CATHY: Sorry, without a spouse around the house, there is no easy way to increase your Internal Revenue Code 121 principal residence sale exemption from $250,000 to $500,000.But your son need not be 18 to add his name to your title. Minors can hold title; they just cannot convey title. However, for him to qualify for an additional $250,000 home sale tax exemption, he must own and occupy the home as his principal residence at least 24 of the 60 months before its sale. If you add him to your title now, please be sure you don't plan to sell the house before he becomes 18 when he can convey title.If he is now 16 or 17 years old, and if he will be 18 or older when you plan to sell the home, you could add him to the title now so he can qualify in 24 months for the extra $250,000 principal residence sale tax exemption. Your tax adviser or real estate attorney can give you more details.As for fixing up your home before sale with new carpet and fresh paint, those are two of the most inexpensive and profitable cosmetic improvements you can make. Although I advise against making major renovations before sale, such as kitchen remodeling, which usually doesn't add much net market value, cosmetic improvements usually pay off handsomely.

What Proof Does Home Seller Need of Primary Residence?DEAR BOB: What proof do I need to show a property was my primary residence for three of the last five years so I can take advantage of the $250,000 capital gain exemption when I want to sell it? -- Rick H. DEAR RICK: Just in case the Internal Revenue Service audits your tax return for the year of your principal residence sale, you should be prepared to prove you owned and occupied it at least 24 of the 60 months before its sale (not three of the last five years).Excellent evidence includes paid utility bills in your name, voter registration, auto license registration, nearby employment, local bank accounts, driver's license at the residence address, filing income tax returns from that address, and other indications of principal residence occupancy. For more details, please consult your tax adviser.

Should Home Sellers Vacate Before Selling?DEAR BOB: My husband insists our home will only sell if we vacate it. This would necessitate having two mortgages until our old home sells. What do Realtors advise? I think our house will show well. -- Susan I. DEAR SUSAN: Your listing agent can best answer this question. He or she can objectively advise if your home will sell for top dollar with your furnishings remaining, or if you should move all your "stuff" out.If you have lots of old-fashioned furniture, or if the house looks cluttered, it is best to move out before putting your home on the market for sale. Or if the house has smells, such as from cooking, smoking, or pets, it's best to move out and correct the problems before listing your home for sale.A vacant house without furniture often makes the rooms look bigger, especially if they are freshly painted and have new wall-to-wall carpets or sparkling hardwood floors.Your listing agent can advise if your home will sell easiest by having it professionally "staged" after you move out. Home buyers are notorious for their lack of imagination. Spending a few hundred, or even a few thousand, dollars on "staging" your home for sale can be a very profitable expense.The new Robert Bruss special report, "Pros and Cons of Fast and Slow House Flipping for Big Profits," is now available for $5 from Robert Bruss, 251 Park Road, Burlingame, CA 94010 or by credit card at 1-800-736-1736 or instant Internet delivery at www.BobBruss.com. Questions for this column are welcome at either address.Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

Friday, April 21, 2006

Is it Time to Steer Clear of ARMs?

Here's a column about the wisdom of fixed-rate vs. adjustable-rate loans ...Thursday, April 20, 2006By Scott MessinaNational Realty News

Now that rates have risen from their all time lows, the number of adjustable rate mortgages being originated is on the rise. This of course, is a predictable event that follows every up-tick in rates. After all, with the prices of housing on the rise often an ARM seems like the only way for a customer to afford the same home they could with a fixed rate product only a few months ago.However, the question you should be asking is what is in a home buyer's best interest? Since it’s highly likely rates will never be as low as they were in 2003, chances are that borrowers financing their new home purchase with an adjustable loan will likely be riding the rate trend upwards, not down. As the economy continues to heat up, it is inevitable that the indexes that adjustable-rate mortgages are tied will begin to rise. The net effect will be higher rates and payments for the very same borrowers who selected an adjustable-rate loan over a fixed rate, since they perceived the adjustable as more affordable.Unfortunately, most home purchasers fail to realize that in as little as two to three years, most adjustable programs will actually have a higher payment than if they were to choose a fixed-rate product today. Unfortunately, this will leave many of these new homeowners with a tough choice in the upcoming years: sell their home or face an insurmountable mortgage payment.So when are adjustable mortgages the correct choice? In a downward-moving market, so purchasers can ride their payments lower, or for a home they truly intend to keep short term. Another good time to use an adjustable is if the borrower is in an occupation that will give them large increases in income for the next several years, so their income keeps pace with the rising payments.Messina has been in mortgage lending for more than 15 years.Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

Housing Market to Stay on High Plateau, Industry Chief Predicts

Here's an article about the future of real estate ...Thursday, April 13, 2006Market expected to be third-highest in historyNational Realty NewsWASHINGTON, D.C. – Home sales should generally level out and remain at historically high levels, according to the National Association of Realtors.David Lereah, NAR’s chief economist, said mortgage interest rates are trending up but will remain favorable. “Economic growth and job creation are providing a favorable backdrop for the housing market, but rising interest rates have an offsetting effect,” Lereah said. “Home sales will move up and down somewhat over the remainder of the year but stay at a high plateau, meaning this will be the third strongest year on record.” He expects the 30-year fixed-rate mortgage to rise to 6.9 percent by the end of the year.Growth in the U.S. gross domestic product is forecast at 3.7 percent in 2006, while the unemployment rate should average 4.8 percent.Existing-home sales are projected to drop 6 percent to 6.65 million this year from a record 7.08 million in 2005. New-home sales are likely fall 10.9 percent to 1.14 million from the record 1.28 million last year – both sectors would see the third best year following 2005 and 2004. Housing starts are forecast at 2.00 million in 2006, which is 3.2 percent below the 2.07 million in total starts last year.NAR President Thomas M. Stevens from Vienna, Va., said home prices are expected to cool, but not as much as in earlier projections. “Although housing inventories have been improving, the balance is still a bit more favorable for sellers and annual appreciation remains in double-digit territory,” said Stevens, senior vice president of NRT Inc. “Even so, the market is in a process of normalization – appreciation will return to normal single-digit patterns, providing solid investment returns into the future.”The national median existing-home price for all housing types is likely to increase 6.4 percent this year to $221,700, while the median new-home price is expected to rise 2.3 percent to $242,700.Inflation as measured by the Consumer Price Index is seen at 3.4 percent in 2006. Inflation-adjusted disposable personal income should grow 3.8 percent this year. Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

Thursday, April 20, 2006

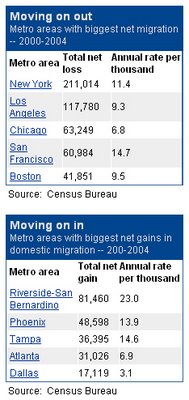

Housing prices make Riverside-SB top destination

Here's a story about how affordable homes here are attracting thousands ...Thursday, April 20, 2006Housing prices put Americans on the moveResidents are leaving high-priced markets in the Northeast and West Coast for more affordable places in the Sun Belt.

By Les ChristieCNNMoney.com staff writerNEW YORK -- The movement of Americans from north to south is trending as strong as ever, according to the latest report on net domestic migration released today from the Census Bureau. And, it seems, housing prices are driving the trend. The net out-migration of residents is from high-priced northeastern and West Coast cities to more affordable housing markets in the Sun Belt."Many are surmising that housing values are so different around the country that it's impacting migration," says Marc Perry, a demographer with the Census Bureau. "Some people are cashing out housing and moving to cheaper areas. Others who don't own homes are moving so they can afford to buy one."That makes losers out of metro areas like New York, Los Angeles and Chicago, and makes Dallas, Atlanta and Phoenix, where housing has been much more affordable, into big net gainers. And, it seems, housing prices are driving the trend. The net out-migration of residents is from high-priced northeastern and West Coast cities to more affordable housing markets in the Sun Belt."Many are surmising that housing values are so different around the country that it's impacting migration," says Marc Perry, a demographer with the Census Bureau. "Some people are cashing out housing and moving to cheaper areas. Others who don't own homes are moving so they can afford to buy one."That makes losers out of metro areas like New York, Los Angeles and Chicago, and makes Dallas, Atlanta and Phoenix, where housing has been much more affordable, into big net gainers.

Loss leadersOf the 25 largest metro areas, the New York region lost the most people, a net outflow of 211,014 residents from the beginning of 2001 through the end of 2004. That calculates to an average loss of 11.1 people per thousand per year. The median house price in the New York area last year was $427,600, about twice the national median.Los Angeles, where home prices averaged $568,400, had a net domestic outflow of 117,780 during the same period, 9.3 per thousand a year. The net out-migration from the San Francisco metro area ($718,700) was even stronger, averaging 14.7 per year for a total of 60,984.Many Angelenos relocated to the "Inland Empire" of Riverside-San Bernardino-Ontario, about an hour east of L.A. Housing prices there were a big draw; the median home cost $392,300, nearly $175,000 less than L.A. That helped the area record a net influx of 81,460 people, for an average annual rate of 23 per thousand. The Riverside metro area was the No. 1 gainer in the United States, both in total numbers and in rate and is now the 13th most populous in the United States, surpassing such better-known metro areas as St. Louis, Cleveland and San Diego.Other areas fattening up on domestic migrants include Phoenix, where the median house cost $268,400, with a gain 48,598, Tampa ($223,000) at plus 36,395 residents and Atlanta ($170,200) with an influx of 31,026. Only seven of the top 25 largest metro areas were net winners; 18 had a net outflow of domestic residents.Among the states, New York had the highest out-migration – 182,886 – and its average per thousand of 9.6 trailed only the District of Columbia, which averaged 18.1.As for net gainers, the Sunshine State leads the pack."Florida has been a sponge for migrants," says Perry. It has attracted more residents than any other state, a net gain of 190,894 (a lot of them retiring or relocating New Yorkers), but Nevada had the highest average annual increase per thousand, 23.3.

Is Florida peaking?There is some evidence that retirees may be starting to shy away from the storms and flood problems that Florida has endured the past few years, especially with real-estate prices there going through the roof. Anecdotal evidence suggests that some retirees are moving to areas in Tennessee, Kentucky and western North Carolina that are considered safer, cheaper and less crowded."We call them halfbacks," says Perry. "They move all the way down to Florida from the North and then move halfway back."Soaring prices in some Florida cities could slow or reverse the net migration there.Migration seems to be at least somewhat independent of economic conditions. In Massachusetts, for example, out-migration has occurred at more than a 50 percent higher rate the past few years than in the decade before, according to Perry. Yet the state suffered much more economic distress in the 1990s than it has in the 2000s.Like virtually every other post-war trend, the attitudes and behaviors of baby boomers is crucial, because of the sheer size of the group."Like Californians," says Perry, "anything they do resonates with the rest of the country. What they decide to do when they retire will have a huge impact on domestic migration."Many of the net losers in this domestic dance have still gained population due to immigration from foreign lands. New York, for example, is one of the six states - others are California, Florida, New Jersey, Illinois and Texas - that in 1990 acounted for three-quarters of all immigrants living in the United States, according to Barbara Lipman, director of research for the Center for Housing Policy.But by 2000, those states could only claim two-thirds of all foreign born U.S. residents, a sharp decline. "These are still the 'gateway states,'" says Lipman, "but 22 other states are seeing significant growth of immigrant populations."If that trend continues, the net-migration loss states may find it even harder to hold onto their populations.See housing prices for 145 metro areas.

Best places to live.Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

Cash-strapped homeowner gets advice on property repairs

Here's an article for those who have a home in need of repairs ...Home equity line of credit may be answer to monetary issues

Thursday, April 20, 2006By Ilyce R. GlinkInman NewsQuestion: I have lived in my house for 10 years and it needs some major repairs, including septic tank problems, possible foundation problems, and other big-ticket items.I never did much maintenance to the house through the years due to marital problems and financial difficulties. My credit isn't the best, so I cannot get a home equity line of credit.I'm thinking of selling, but I know I will sell the house for a loss and maybe get stuck owing cash on the mortgage. What can I do? Thank you.Answer: You're in a difficult situation financially, without a lot of options. But, you may have more than you think.First, get a copy of your credit history and credit score through www.annualcreditreport.com. You're entitled to a free copy from each of the three credit reporting bureaus. When you go there, you'll be asked if you'd like a credit score. You'll pay $6.95 for this, but it's a good value. You'll see what lenders are going to see.Next, talk to some top-rated mortgage lenders, such as a national company, a big local bank, a local credit union, and a mortgage broker you know and trust. For the national companies, you can go to JD Power and Associates (www.jdpower.com) to see which companies rank highly for customer service.These companies are well qualified to tell you what kind of interest rate you'd qualify for and how much you'd pay for a home equity line of credit.What most folks don't understand about credit these days is that almost no one is turned down. Although your credit score may not be the highest, it may be good enough to get a line of credit or a home equity loan at a fairly decent rate.If you can refinance your mortgage and take out some of the equity that you have, you may be able to do some of the repairs and improvements you need to do to continue living there.It's also possible that the house and its problems aren't worth saving and the value of your property is in the land. Talk to a local real estate agent about what's going on in your neighborhood in terms of teardowns. Hopefully you can sell the house for at least what your mortgage balance is.Finally, if you are going to sell and you'll be in a short-sale position (that is, the house is worth less than the mortgage balance), know that you're going to get a tax bill for the difference between what you owe and what the bank settles for, the following April 15th.The Internal Revenue Service treats short sales as phantom income, and you'll be expected to pay tax on the difference between what you owed and what the bank accepted. For example, if you owe $50,000 on the property, but the house sells for $40,000, and the bank agrees to take $40,000 and close out your account, the IRS will treat the missing $10,000 as income and you will pay federal and state tax on that amount.It sounds unfair, but that's the law. You've got some work to do here, to figure out which direction will be best for you. It won't be easy, but I know you can get through it.Contact Ilyce through her Web site, www.thinkglink.com.Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

Wednesday, April 19, 2006

Riverside County home sales continue to climb

Here is a story about the local real estate market ...Riverside the only SoCal county to see increase from last year; sellers find themselves in a crowded marketWednesday, April 19, 2006By LESLIE BERKMANThe Press-Enterprise

Sales of homes in March increased again in Riverside County compared with a year ago, even as the number of sales in Southern California decreased for the fourth consecutive month, a real estate information service reported Tuesday.The Inland Empire housing market's ability to buck the Southern California trend was attributed to its greater affordability, as the Southland's median home price for the first time passed $500,000, according to a study by DataQuick Information Services.Last month, Riverside County posted 6,267 home sales, 6 percent more than in March 2005, while the county's median home price in the same period rose 9 percent to a record $413,000.Among the six counties in Southern California, Riverside alone saw a year-to-year increase in sales. The most severely impacted was Orange County, where the number of sales fell by more than 22 percent.New-home sales in Riverside County were particularly brisk in March, hitting 2,742, the second biggest on record for the area's builders, said John Karevoll, an analyst with DataQuick, which compiles and publishes monthly housing data.San Bernardino County in March saw year-to-year sales drop 3.4 percent, while its median home price of $367,000 fell short of February's record $373,000 but was 23.2 percent higher than in March 2005.San Bernardino County's year-to-year appreciation rate was the largest gain in the region. The average appreciation for Southern California was 14.1 percent.Karevoll said March, traditionally a bellwether month for housing forecasts, turned out "a bit stronger than we anticipated. We would have thought a year ago that by now appreciation for the region would have been in the single digits."Still, Karevoll said it is clear that the Southern California housing market is cooling off, led by the coastal counties."Overall things are slowing down, but they are slowing from what was basically a very strong, if not frenzied, market," Karevoll said.For the first time in three years, Karevoll said, the supply of housing and buyer demand has come into balance, ousting sellers from the driver's seat.The Multi-Regional Multiple Listing Service, which tracks resales in the San Gabriel Valley and the Inland region, said in the first quarter the number of houses on the market soared 185 percent to nearly 21,000.The combination of a high number of new listings and declining sales, the service said, created a 6.9-month supply of homes with "for sale" signs at the end of March, up from 2.4 months a year earlier.Leslie Appleton-Young, chief economist for the California Association of Realtors, said the number of homes available for sale a year ago was extraordinarily low a year ago and is now closer to the historic average.Appleton-Young said although the pace of home appreciation has slowed, she didn't foresee a decline in the median home price as long as the economy stays strong. She said as long as people are employed they are not forced to sell their homes.Charles Chacon, an agent with Re/Max Allstars in Corona, said the market is softening because there aren't enough motivated buyers to absorb the wave of new listings."As interest rates edge up a little people get nervous," Chacon said. "Buyers get cautious because they think it will get cheaper a year from now, and sellers panic because they think we are at the top, and we very well could be."Beth Collins, one of Chacon's clients, said she and her husband, Dale, put their 5-bedroom house in Corona on the market in late January but still haven't found a buyer although they lowered their price by $10,000 to $639,900. Collins, 50, said the couple wants to move to a small town in Iowa to be close to her parents. But she said they are in no rush."As you drive around town there are a lot of houses for sale," Collins said. "I feel lucky that we don't have a deadline."Art Del Rio, 51, said he and his wife, Cyndi, are eager to sell their Corona townhouse and tried to price it below the competition because they have a contingency offer to buy a single-family detached house in Canyon Crest. He said he had expected that at $399,900, their three-bedroom townhouse would sell in two weeks."We are pushing a month now, and although we have had a lot of people come through with agents, they just aren't buying," Del Rio said."As late as October the homes in this development were selling literally within days of being available for sale. We had an agent twice knock on our door wanting to know if we wanted to sell. But then we weren't thinking about it." Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

Monday, April 17, 2006

Housing market headlines can be misleading

Here's an article about the sensational real estate headlines that are prevalent today ...

Location affects how real estate market behaves

Monday, April 17, 2006

By Dian Hymer

Inman News

On Jan. 20, 2005, a headline in the San Francisco Chronicle stated that Bay Area home sales were down and that prices slid. If you, like many readers, scanned only the headlines, you might have thought home prices in the area had plummeted. Actually, they rose 14.3 percent between December 2004 and December 2005, according to DataQuick Information Systems.

Sensational headlines sell newspapers. Who wants to read about a real estate market that's not as robust as it was a year ago -- one in which home prices aren't going up as fast as they were this time last year? Ho-hum news doesn't do much for newspaper sales.

Behind the scenes of the Bay Area home sale market, the real story is not that home prices "slid" from one month to the next. It's that the market is doing surprisingly well despite the negative press. In a nutshell, well-priced homes that are properly prepared for sale are selling for good prices and within a reasonable period of time.

While this is not the case in all markets, it certainly holds true for markets that are low on inventory. Recently, a home in a moderately priced neighborhood in Los Angeles sold with 10 offers. This miraculous event occurred in February 2006, not February 2005.

Areas that are flush to overflowing with unsold listings are a different story. These are areas that were overbuilt during the last five years. New-home builders in these areas are offering concessions, like free landscaping and other upgrades, to encourage sales. Sellers of resale homes in over-built areas are forced to cut their prices in order to compete.

HOUSE HUNTING TIP: Regardless of where you live, there are two factors to keep in mind when evaluating news reports on current market conditions. One is that you need to evaluate what's happening now in relationship to what came before. We've recently experienced several of the best years for home sales on record. If the market were to continue to escalate, we'd have a serious problem.

Already, we have affordability issues, given the recent rise in home prices. If home prices were to continue to rise unchecked, first-time buyers would eventually be shut out of the market. With no entry-level buyers, the move-up market would grind to a halt. Rather than a curse, the slow-down in the housing market is a blessing.

The other factor to keep in mind when you're trying to make sense of changes in home prices is that, in most cases, the changes quoted in the press are changes in the median price of homes sold during a given period of time. The median price is the price that is halfway between the highest-priced and lowest-priced home sold in that period.

Changes in median price from one period to the next do not necessarily reflect changes in absolute home values. When the median price rises, it means that the number of more expensive homes sold during that period increased. Likewise, when the median price of homes sold declines, this means that the volume of lower priced homes sold increased relative to the number of more expensive properties.

Following the dot-com bust in 2000, the median home price in the San Francisco Bay Area dropped. This was due to the fact that the market for more expensive properties dried up. However, the market for properties priced under $1 million remained strong.

THE CLOSING: Before drawing conclusions about the strength of the home sale market in your area, you need to collect data at your local level. Regional, statewide and national statistics can be misleading.

Hymer is author of "House Hunting, The Take-Along Workbook for Home Buyers," and "Starting Out, The Complete Home Buyer's Guide," Chronicle Books.Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

Wednesday, April 12, 2006

Despite risk,most Californians skip quake insurance

Here's an eye-opener ...Tuesday, April 11, 2006By Jim ChristieReuters News ServiceSAN FRANCISCO -- With the 1906 San Francisco earthquake very much in the public eye ahead of its 100th anniversary next week, interest in insurance against future quakes remains remote for many Californian homeowners.Just 14 percent of homeowners in the temblor-prone state have earthquake insurance, according to state officials, creating considerable financial uncertainty for a state where future catastrophe waits just beneath the Earth's surface."The vast majority of people know an earthquake is likely to occur but willingly turn down the coverage," said Robert Hartwig, chief economist for the Insurance Information Institute, a trade group for insurers. "They're playing Russian roulette."While insurance carriers must offer California homeowners earthquake insurance and the insurer-funded California Earthquake Authority also offers it, the state's households overwhelmingly prefer to go without -- despite dire warnings about the potential for earthquakes.Even top earthquake experts are among the earthquake insurance have-nots.University of California at Berkeley seismologist Robert Uhrhammer is retrofitting his wood-frame home, which is about two miles from a fault capable of magnitude 7 earthquakes, to bring it up to current earthquake codes. Yet he opted against earthquake insurance."I expect it would fare well even through the strongest shaking, with little or no structural damage," he said.Such thinking calculates that wood-frame homes withstand earthquakes fairly well and mitigating financial risks to them may be best accomplished with measures other than insurance.Others say it's better to be financially prepared for the worst, a potential earthquake known simply as "The Big One.""People living in California know they are living in earthquake country but I'm not sure they know the risk in a quantifiable way," said Jayanta Guin, vice president for research and modeling for risk-modeler AIR Worldwide Corp.Seismologists estimate the 1906 earthquake that struck San Francisco was a magnitude-7.8, marking a major temblor. The U.S. Geologic Survey estimates a 62 percent probability of a magnitude-6.7 or greater earthquake capable of causing widespread damage striking the San Francisco area before 2032.Guin's company estimates the current value of residential and commercial property in the "damage footprint" of the 1906 earthquake at more then $1.6 trillion. Were a temblor similar to the 1906 earthquake to strike the area there would be estimated insured property losses of $80 billion and total property losses would top $300 billion, according to AIR.The numbers argue for Californians who live along or near earthquake faults to buy insurance to protect against the catastrophic loss of property, said Nancy Kincaid, a spokeswoman for the California Earthquake Authority.She stresses the word "catastrophic" because the cost of repairing substantive earthquake damage to a house and maintaining mortgage payments could wipe out many homeowners."Most consumers don't have a good reality check on how they would recover," Kincaid said, noting homeowners may buy the authority's catastrophic insurance for between $200 and $2,000 a year depending on where they live and the type of home.Californians foregoing earthquake insurance, however, may be making an informed choice because serious earthquakes are rare and deductibles on the policies are high -- 10 percent to 15 percent of a home's insured value -- so cosmetic damage likely would not be compensated. Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

Tuesday, April 11, 2006

New homes aren't always perfect

Here's an article about new homes and the need for a pre-close inspection ...Builder's warranty may save owners who didn't do pre-purchase inspectionTuesday, April 11, 2006By Barry StoneInman NewsDear Barry: In a recent column, you recommended home inspections for brand-new homes. This was eye-opening advice for us, but unfortunately, we learned it too late. We bought a brand-new home about six months ago and assumed there was no need for a home inspection.The building department had just approved the construction, and the home was covered by a one-year builder's warranty, so we saw no need for an inspection. Our new neighbor, on the other hand, did hire a home inspector. Nearly a dozen defects were reported, and the builder repaired all of them. This makes us wonder what a home inspector would have found in our house. Now that we've taken possession without an inspection, what do you recommend? -- Bill and Anne Dear Bill and Anne: A pre-purchase home inspection is essential when buying a brand-new home, but don't despair. The window of opportunity is not yet closed because the builder's warranty is still in effect. The contractors who built your home are still required to correct any defects that you discover and bring to their attention. What matters now is that these discoveries be made.As stated in previous articles, most purchasers of new homes fail to obtain a professional inspection. Instead, they trust that new homes are unlikely to have defects and that any imperfections will inevitably become apparent during the warranty period. These two assumptions have caused financial loss and mournful regrets for many buyers of new homes. "Brand-new" means clean, shiny, unworn, aromatic, and sanitary. It does not mean defect-free. The Trojan horse was brand new, but it should have been inspected. Homes are built by people, and regardless of experience, skill, knowledge, integrity, and good intentions, all people make mistakes. That's the one guaranty that never fails.Then there is the question of building department approval. Municipal building inspectors provide services that are limited by the time available to perform an inspection. Building departments are typically under-staffed and over-worked. An inspector might have as little as 15 minutes to evaluate a home. Furthermore, municipal inspectors have no liability for defects that are missed during their inspections. Therefore, the motivation for thoroughness is missing.With home inspectors, the situation is much different. A competent home inspector spends two-and-a-half to four hours on-site, time enough to access and inspect all pertinent areas of the home. As members of the private business sector, home inspectors do not enjoy the liability protections that shelter bureaucratic agencies and their employees. Hence, they are motivated to perform thorough, comprehensive inspections.A competent home inspector -- someone with years of experience, substantial credentials, and a reputation for thoroughness -- can provide valuable financial protection to the owners of new homes. The missing ingredient is public awareness of the need to inspect newly built homes. As long as the warranty period is in effect, owners can present a list of repair needs to their builder. When the warranty expires, the opportunity is lost. Defects discovered after that time become the homeowner's responsibility.

To write to Barry Stone, please visit him on the Web at www.housedetective.com.Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

Wednesday, April 05, 2006

Second-Home Sales Hit New Record in '05

Here's an interesting article about the second-home market ...Wednesday, April 5, 2006National Association of RealtorsSales of vacation homes and investment homes set new records in 2005, with the combined total of second-home sales accounting for four out of 10 residential transactions, according to the National Association of Realtors.The annual report, based on two surveys, shows that 27.7 percent of all homes purchased in 2005 were for investment and another 12.2 percent were vacation homes. All together, there were 3.34 million second-home sales in 2005, up 16 percent from an upwardly revised total of 2.88 million in 2004. The market share of second homes rose from 36.0 percent of transactions in 2004 to 39.9 percent in 2005.Vacation-home sales increased 16.9 percent last year to a record 1.02 million from a downwardly revised 872,000 in 2004, while investment-home sales rose 15.7 percent to a record 2.32 million in 2005 from an upwardly revised 2.00 million in 2004.David Lereah, NAR’s chief economist, says all the factors at play in the second-home market were favorable in 2005.“To begin with, the baby boom generation is driving second home sales – they’re at the optimum point in life when people become interested in second homes, they’re at the peak of their earnings, interest rates remain historically low and boomers want to diversify investments,” Lereah said.There are significant motivational differences between vacation-home buyers and investment buyers, he added.“Vacation-home buyers are making lifestyle choices and purchasing primarily for their own enjoyment,” he said. “Investment-home buyers are seeking rental income and portfolio diversification, although vacation-home buyers also mentioned diversification.”What factors are driving second-home purchases? For vacation-home buyers, 41 percent plan to use the property for vacations, 31 percent to use as a family retreat and 28 percent to diversify investments, according to an NAR survey. For investment-home buyers, 55 percent are seeking rental income and 35 percent want to diversify investments.The median price of a vacation home in 2005 was $204,100, up 7.4 percent from $190,000 in 2004. The typical investment property cost $183,500 last year, up 24 percent from $148,000 in 2004. NAR President Thomas M. Stevens from Vienna, Va., said not all second-homes sales are necessarily a second home: “Some of these purchases may be a third, fourth or fifth investment property, showing that housing is a good investment,” said Stevens, senior vice president of NRT Inc. “The lion’s share of investment homes is actually the primary residence of a renter. Most investment owners are seasoned buyers who understand the long-term benefits of ownership, but not everybody is cut out to be a landlord.”Four percent of all home owners hold three or more properties; 11 percent own two properties.Typical vacation-home buyers in 2005 were 52 years old, earned $82,800, and purchased a property that was a median of 197 miles from their primary residence. However, 47 percent of vacation homes were less than 100 miles and 43 percent were 500 miles or more. Investment-home buyers last year had a median age of 49, an income of $81,400, and bought a home that was close by – a median of 15 miles from their primary residence.More than three-fourths of vacation-home buyers have no interest in renting their property, and 21 percent say it would become a primary residence on retirement, compared with only 2 percent of investment buyers. Fourteen percent of investment buyers and 6 percent of vacation-home buyers purchased a property that their son or daughter can occupy while in school.In describing characteristics that vacation home buyers value about their property, 40 percent want to be close to an ocean, river or lake; 34 percent close to family members; 27 percent close to preferred recreational activities; 27 percent close to their primary residence; 26 percent close to mountains; 24 percent close to a preferred vacation area; and 17 percent close to a job or school.Activities of interest that affected the decision to buy a particular vacation home include beach, lake or water sports, cited by 37 percent of buyers; golf, 29 percent; theme parks, 18 percent; winter recreation, 16 percent; hunting or fishing, 12 percent; and boating, 9 percent. Smaller categories included gambling; biking, hiking or horseback riding; and tennis.The largest concentration of vacation-home buyers are in the Midwest, accounting for 33 percent of vacation home sales, although the property may be located in another region. Buyers in the South accounted for 30 percent of vacation-home transactions, the West, 20 percent, and the Northeast, 17 percent.Most investment-home buyers are in the South – 38 percent of the total. Buyers in the Midwest and Western regions each purchased 24 percent of investment property, and the Northeast, 15 percent.One-third of vacation-home buyers and 36 percent of investment-home buyers said it was very likely that they would purchase another home, in addition to properties currently owned, within the next two years.Lereah said it is difficult to project where the market will go in 2006.“Vacation-home sales will remain strong for the foreseeable future given the fact that baby boomers are favorably positioned in terms of affordability, as well as being at the stage in life when people are most interested in making that kind of a lifestyle purchase,” he said. “Discretionary purchases of that nature are more likely in a healthy economy, and that is looking positive as well.“On the other hand, investment-home sales are likely to decline this year, in part because of higher interest rates,” Lereah said. “There are fewer incentives to speculate in the market with price appreciation cooling in much of the country, and more oversight is being encouraged in the mortgage market. It’s hard to say how much speculation there may be in housing, but it’s probably a single-digit percentage of total home sales.”NAR survey data show only 2 percent of homes are sold in one year or less, but investment homes likely are under-represented in that particular reporting sample.Lereah expects a soft landing for the housing sector in 2006 with existing-home sales declining 5.7 percent to 6.67 million, the third-highest on record. “Long term, the outlook for second homes is favorable because more people will be moving into the prime years for buying a second home,” he said.Currently, there are 36 million people age 50 to 59. However, there are 45.2 million people age 40 to 49. “That younger segment will become a driving force in the second-home market over the next decade,” he said.The second-home report is based on two surveys. One, to determine market share and to extrapolate sales data, was conducted in March 2006 of a panel of recent home buyers. That survey captured data for 3,406 home buyers in 2004 and 2005, with roughly equal samples for each year; data were weighted to correspond with demographic findings in an earlier mailed survey.To determine median home prices, most of the demographics and buyer preferences, NAR mailed an eight-page questionnaire to a national sample of 145,000 buyers who purchased their homes between mid-2004 and mid-2005 based on county records. It generated 7,813 usable responses; the response rate was 5.4 percent. Data in this report only includes data from respondents who indicated that they purchased a vacation home or investment property. A more extensive study, The 2006 National Association of Realtors Profile of Second Home Owners, currently is underway and will be released in late spring. This study will be based on a large sample of existing owners and will update NAR’s benchmark study of second home owners that was published in 2002.For more housing market statistics and research reports,visit NAR's Research Department at www.realtor.org.Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

Tuesday, April 04, 2006

No Housing Bubble Found in 9 of 10 Urban Markets, Study Shows

Here is an interesting article about a study on real estate prices ...Monday, April 3Ascribe NewswireCLAREMONT -- Fears of a real estate bubble are overblown, and homes remain undervalued in many markets, according to new research from a pair of Pomona College professors who developed a fresh methodology for gauging bubble trouble. By comparing the cash flow generated by owning a home to the cost of renting a comparable house, economics professors Gary Smith and Margaret H. Smith found bubble conditions in only one of the 10 metropolitan U.S. housing markets evaluated.

In a paper presented March 31 at the Brookings Institution in Washington, D.C., the husband-and-wife team concluded that buying a home generally remains an attractive long-term investment -- even if buyers are conservative in their assumptions about how much home prices will rise in the future.

"Most of the country is certainly not in a bubble if you define a bubble as prices far above fundamentals," said Gary Smith, who is the Fletcher Jones Professor of Economics at Pomona College. "The average person in the U.S. is still better off buying than renting."

San Mateo County in the San Francisco Bay area was the only region studied where homes were overvalued, and that was by 54 percent. Elsewhere in California, Orange County prices were about right, while homes in Los Angeles and San Bernardino counties still were somewhat undervalued, 11 percent and 20 percent, respectively. Beyond California, homes also were undervalued in Boston (12 percent under) and Chicago (17 percent under). Undervaluation was dramatic in Dallas (40 percent), Atlanta (53 percent), Indianapolis (65 percent) and pre-Hurricane Katrina New Orleans (46 percent).

The Smiths' methodology consisted of evaluating housing as a long-term investment, similar to stocks and bonds. In each market they studied, the Smiths matched up similar homes, comparing the cost of buying vs. renting, using Multiple Listing Service data from summer 2005. They projected homeowners' net savings on rent over time, discounted by a required after-tax rate of return of 6 percent, because the money sunk into the home purchase could presumable be invested elsewhere, for example, in stocks and bonds. Their analysis factored in expenses such as one-time closing costs, taxes, maintenance and insurance. On the other side of the ledger, they also factored in tax benefits from ownership and the fact that rents will rise over time, while payments on a fixed-rate mortgage will not.

They assumed a 20 percent down payment, with a 30-year mortgage at a 5.7 percent fixed rate. Under the Smiths' model, in many cases, the home purchase initially generates negative cash flow, as the expenses of owning exceed the rental value and tax benefits. But over time cash flow becomes positive. And in some of the more dramatically undervalued markets, such as Indianapolis, owning a home generated an immediate positive cash flow.

So why all the talk about a housing bubble? The Smiths note in their paper that as housing prices have risen dramatically in recent years, some researchers have concluded that homes are now priced well beyond their fundamental values. But the Pomona College professors question the implicit assumption that market prices previously matched fundamental values but now have exceeded them. "Perhaps housing prices were too low in the past and recent prices have brought market prices more in line with fundamentals," they write.

Beyond that, the Smiths question the methodology by which some researchers have concluded that the housing market is "bubbly." The report notes that "housing-bubble discussions generally rely on indirect barometers such as rapidly increasing prices, unrealistic expectations of future price increases, and rising ratios of housing price indexes to household income indexes. These indirect measures cannot answer the key question of whether housing prices are justified by the anticipated cash flow."

Gary Smith says their model also can be adapted to calculate the likelihood of housing being a good investment under different scenarios, such as an adjustable-rate mortgage instead of a fixed. However, the Smiths' model assumes buyers will hold on to the house for the long haul, not selling in a couple of years.

He advises against trying to predict which direction home prices are headed, telling the cautionary tale of a Claremont professor who in 2003 decided against buying because he had read in the newspaper that home prices were 20 percent too high. It turns out home prices rose dramatically in the area. Prices instead continued to rise dramatically. "You've got to run your own numbers," Smith said.

Gary Smith is the author of more than 50 articles and several economics textbooks. He earned his B.A. in mathematics at Harvey Mudd College and his Ph.D. in economics at Yale University. Margaret H. Smith, an assistant professor of economics at Pomona College, earned her B.A. at Yale University and her Ph.D. at Harvard University (both in economics). She also is a Certified Financial Planner and has been published in journals such as the Journal of Financial Planning, Applied Financial Economics and Industrial Relations.

Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

Final walkthrough recommended before real estate purchase

Here's an article about the perils of not doing a pre-close walkthrough ...Defect discovery could put deal on hold, re-open negotiations

Tuesday, April 04, 2006By Barry StoneInman NewsDear Barry,

Before we bought our home, the entire place was jam-packed with stuff, not just throughout the house, but in the garage and around the outside of the building as well. The sellers disclosed a few problems--a leaning retaining wall and a crack in the driveway--but it was hard for our home inspector to find much else, owing to the clutter. Once we moved in, the impact of this became clear. Now we can see the bulge in the garage foundation, signs of settlement in the rear bedroom, mold on the walls, and a list of other defects. Even with a home inspection, we bought the house sight-unseen. How could we have prevented this, and what can we do now? -- JoeDear Joe,As a condition of the sale, just prior to closing, the seller should have vacated the property to enable a final walkthrough inspection. A walkthrough is standard procedure when buying a home, ensuring that no vital areas of the property are concealed from sight and that no defect discoveries are unreasonably prevented. Had this routine process taken place, the foundation problems, the mold issue, and various other defects would then have been apparent. Had there been a walkthrough, a list of property defects that should have been disclosed by the sellers would then have come to light, the purchase could have been put on hold, and negotiations with the sellers could have been re-opened. Instead, concealed defects were purchased on faith, and you have been left with an armload of costly surprises.On the basis of disclosure requirements, the sellers are clearly in the wrong. They should have informed you of all visible defects. Even if they were unaware of problems concealed behind their clutter, obvious flaws would have been revealed to them when they finally removed their mess. Whether early or late in the transaction, it was their obligation to divulge whatever they knew to be problematic.Now that the milk is spilt, your options are limited. To begin, the newly discovered defects need professional evaluation, including an engineering review of the foundation and cost estimates for necessary repairs. Finally, you'll need to inform the sellers of the newly revealed status of the property and to request that they contribute to the repair process. If they are not willing to pay for undisclosed defects, you'll have to consider whether legal action is worth the additional cost and aggravation.

Dear Barry,When we bought our home, the seller agreed to repair the roof. But winter weather prevented this at that time. So the seller left money in an escrow account to pay for later work. Here's my question: I'm able to do my own roof repairs and would like to save money by doing the job myself. How can I get approval for this kind of arrangement? -- Andrew

Dear Andrew,The money being held in escrow is apparently part of the seller's proceeds from the sale of the property. Any savings in the course of roof repairs would thereafter be refunded to the seller. Accordingly, the seller may welcome your offer to make these repairs. However, you will need to assure the seller, in writing, that there will be no further claims if your roof repairs are in any way unsuccessful. You need to make a proposal to the seller to see if your intentions are mutually agreeable.To write to Barry Stone, please visit him on the Web at www.housedetective.com.Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

Saturday, April 01, 2006

Is lease with option to buy wise for property owner?

Here's a great column about the wisdom of lease-option purchases ...How arrangement works for seller and buyer

Thursday, March 30, 2006By Ilyce R. GlinkInman NewsQUESTION: I own a property and am considering a lease with an option to buy instead of just leasing the property. I have a mortgage on the property, and I'm wondering if I can do a lease-purchase on the property to someone even though the property is mortgaged? I pay the mortgage on time each month.ANSWER: If you own the property, you can do a lease-option, which allows the renter to accumulate some down-payment money as well as have an option to purchase the property at some point in the future.Leasing this rental property is acceptable. The only different thing is that typically with a lease-option, you would negotiate the purchase price at the beginning of the lease/option period.If the option is picked up, all you need to do is schedule the closing date, hire an escrow or title company, and provide any state-mandated disclosure. Unless your loan is assumable (meaning that the future buyer can assume the mortgage from you), you will have to pay off the mortgage with the proceeds from the sale.The buyer will have to get approved for a loan in his or her own name. And that's typically the reason why many first-time buyers want to do a lease-option -- they can't quite qualify to buy the home that they've decided they want.Doing a lease/option allows the buyer to live in the home for a year and pay a non-refundable option for the right to purchase the property in the future at a price that's negotiated today.Finally, most home loans do not prohibit you from leasing your property and usually require you to pay off the loan upon the sale of the home.QUESTION: Before I meet with an exclusive buyer's agent or check out homes, should I get pre-approved for the maximum amount or for the price range I'm interesting in purchasing?I spoke with the exclusive buyer's agent I'm thinking about using yesterday and he told me not to get pre-approved for the amount I'm thinking about offering, but to go ahead and get pre-approved for the maximum amount.My only concern is that if the buyer's agent shows the listing agent my pre-approval letter noting the maximum amount the lender is willing to finance, I think it will eliminate my leverage when it comes time to negotiate with the seller.Anyway, my gut is telling me that the buyer's agent is looking to get the highest amount for the property, thus a higher commission. What are your thoughts?ANSWER: Real estate attorneys confirm that brokers are including pre-approval letters along with purchase contracts. So you're right to be concerned. But I think there is a relatively easy way to get around this problem.But first, in general, I don't think you should tell anyone how much money your lender has agreed to finance for you. Your agent shouldn't know that number specifically nor should the seller's agent or the seller. Playing your financial cards close to the vest is an important part of the negotiation of the sales price. You alone should know how much you can ultimately afford to spend on a home.However, your agent needs to know how much you're willing to spend on a property--and that can be an entirely different number.You need to decide how much you're willing to spend each month, a number that I would hope will be based on your current personal finance situation--how much you're bringing home, how much you're paying out in monthly debt service, and how much you've already saved for the down payment.Once you tell the agent you're willing to spend, say, $250,000, she should show you homes that are priced not too much above that number. But telling her that's what you're willing to spend is different from showing her a pre-approval letter that states the lender is willing to loan you up to $300,000.If you've decided that $300,000 is too much for your budget, it doesn't matter that the lender thinks you should be able to afford it. You may not feel that way. And showing that letter to your agent -- even an exclusive buyer's agent -- could change the dynamics of your home buying experience.Here's one possible solution. Find out how much your lender would be willing to lend you--the maximum loan possible. Then, add in how much down payment you have for the purchase. Finally, decide if that's the total amount you really want to spend.Once you decide what is the maximum amount you want to spend on a home, ask the lender to prepare a pre-approval letter for 80 percent of that amount. The lender will assume that you'll be putting down 20 percent on the property. If you decide later to get a loan with a smaller down payment, say 10 percent, you will still fall within the guidelines of what the lender originally agreed to lend to you.But when your agent clips a copy of the pre-approval letter to the purchase contract, you're not giving away the store.You can even ask the lender to tailor the pre-approval letter for the home you want to bid on, by working the numbers specific to the transaction.I do want to address one other point in your letter: I don't think a quality buyer's agent will be trying to get you to ante up and spend more for a house just so the commission is slightly larger.Most agents run their businesses by referral so they want you to have the best home-buying experience possible. That way, they hope, you'll think of recommending them to your friends and relatives. That's how they build their businesses and make a living.Judging from the tone of your e-mail, trust sounds like a big issue for you. If you don't trust this agent, then you need to start shopping around for another agent. This is the single biggest purchase of your life and you need to be with someone you can trust to have your best interests at heart.

Contact Ilyce through her Web site, www.thinkglink.com.Labels: Corona, Foreclosure, Home Prices, Inland Empire, Loan Modification, Moreno Valley, Murrieta, Real Estate, Riverside, Short Sales, Statistics, Temecula

|